Who’s Winning and Who’s Being Left Behind

In 2025, the world spent $581 billion on artificial intelligence and data centers. That’s more than double the $253 billion invested in 2024, and well above the previous record of $360 billion set in 2021. The AI investment race isn’t slowing down, it’s accelerating at a pace that is reshaping the global economic order in real time. But here’s what the headline number doesn’t tell you: this race is not even close. One country is so far ahead that the rest of the world is essentially competing for second place. And the gap is widening every year.

This is the story of who’s winning the global AI investment race, who’s being left behind, and what it all means for the future of economic power.

A Race With One Clear Leader

Let’s start with the data.

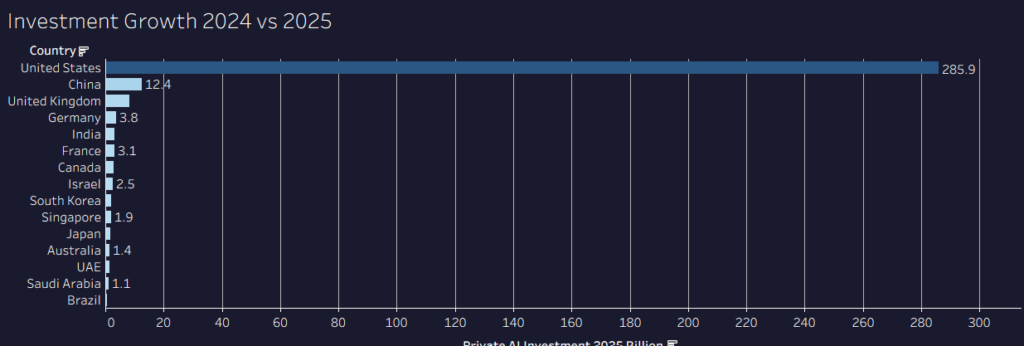

In 2025, the United States invested $285.9 billion in private AI which is more than 23 times China’s $12.4 billion. To put that in perspective: the entire rest of the world combined invested less than the US in a single year. The UK, ranked third globally, invested $8.2 billion which is roughly 3% of the US total. The gap didn’t just persist in 2025, it widened dramatically. In 2024, the US-to-China investment multiple was 11.7x. By 2025, it had jumped to 23x. US AI investment grew 162% in a single year. China grew 33%. The pace difference tells you everything about where momentum lies.

Since 2013, cumulative private AI investment in the US has reached approximately $470.9 billion roughly four times China’s $119 billion over the same period. The US has not just won the early rounds of this race; it has lapped the field.

Porter’s Five Forces —> Why the US Dominance Is So Hard to Challenge

To understand why other countries struggle to close the gap, Porter’s Five Forces framework is illuminating.

Threat of new entrants — Extremely High Barriers. Building competitive AI infrastructure requires not just capital, but a dense ecosystem of talent, compute infrastructure, research institutions, and venture capital networks. The Bay Area alone accounted for nearly 70% of all US AI venture capital in Q1 2025. Replicating that ecosystem from scratch takes decades, not years.

Bargaining power of suppliers — Critical and Concentrated. The most important input for AI advanced semiconductors is produced by a handful of companies, primarily TSMC in Taiwan and NVIDIA in the US. Countries without access to cutting-edge chips face a fundamental constraint on their AI ambitions. China’s semiconductor fund of $47.5 billion reflects exactly this problem, an attempt to break the supply dependency.

Bargaining power of buyers — Growing but Fragmented. Governments and enterprises worldwide are buying AI services, but they increasingly buy from US platforms like OpenAI, Google, Microsoft, Anthropic. This creates a feedback loop: US platforms capture global revenue, reinvest it in R&D, and widen their lead.

Threat of substitutes — Limited in the Short Term. There is no substitute for frontier AI capability. Countries that fall behind cannot simply opt out as AI is becoming infrastructure, like electricity or internet connectivity. The cost of not participating is falling competitiveness across every sector.

Competitive rivalry — Intensifying but Asymmetric. China, the EU, and Gulf states are all investing aggressively, but from very different starting points. The rivalry is real, but asymmetric like a Formula 1 race where one car has a fundamentally superior engine.

The Surprising Outliers

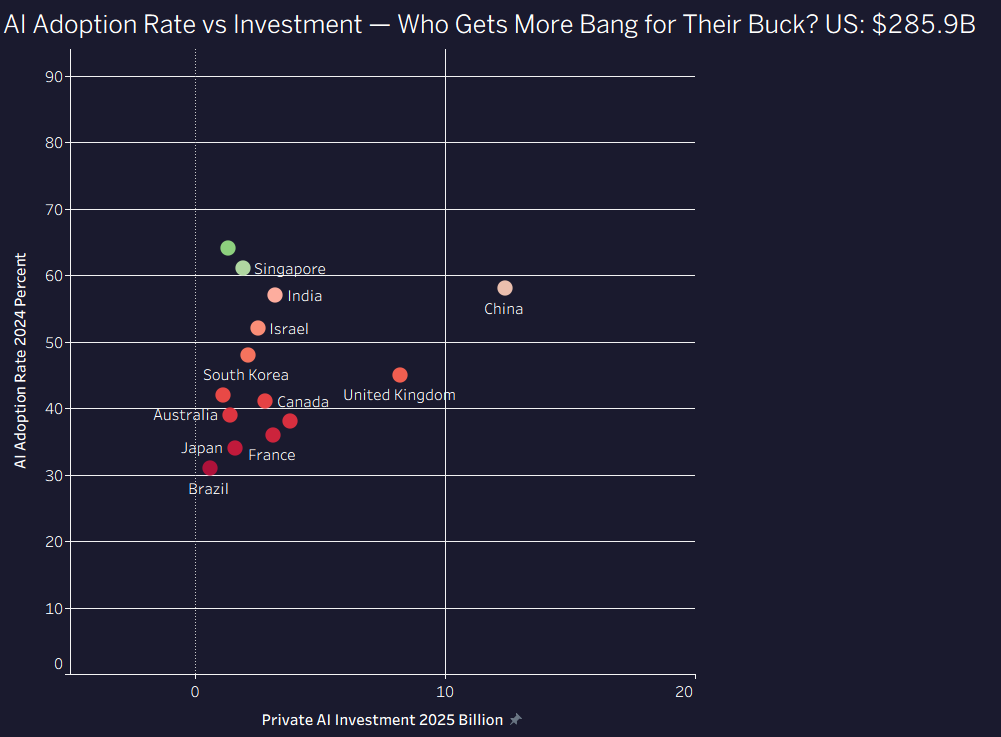

Here’s where the data gets genuinely interesting. When you plot AI adoption rate against investment, a striking pattern emerges. The UAE (64% AI adoption) and Singapore (60.9%) top the global rankings for population-level AI usage, despite investing a fraction of what the US or China spends. India (57%) and China (58%) lead in enterprise AI deployment. These outliers reveal an important distinction: investment and adoption are not the same thing.

The UAE’s Project Transcendence a $100 billion government AI commitment that represents the largest AI pledge outside the US and China. But what makes the UAE interesting is not just the money; it’s the deliberate national strategy to become an AI hub, attracting global talent and companies through regulatory flexibility and government-backed infrastructure.

Singapore’s approach is different but equally strategic: positioning itself as the AI governance and deployment hub for Southeast Asia, leveraging its strengths in financial services, logistics and education.

These small nations are pursuing what business strategists would recognize as a Blue Ocean Strategy that rather than competing directly with the US and China in AI research and development, they’re creating uncontested market space in AI deployment, governance, and regional hub services. They can’t win the arms race. So they’re redefining what winning looks like.

Regulation vs Innovation

Europe presents a fascinating case study in the tension between regulation and innovation. France committed 109 billion euros to AI-related programs a number that sounds impressive until you compare it to the US figure. Germany, the UK, and France combined invested roughly $15 billion in private AI in 2025. The entire EU produced just three notable AI models in 2024, compared to 40 from the US and 15 from China.

Europe’s challenge is structural. Its strength in regulation which is exemplified by the EU AI Act which creates guardrails that protect citizens but also slow deployment. Its fragmented capital markets mean there’s no European equivalent of Silicon Valley’s venture ecosystem. And its talent consistently migrates to the US, where compensation and opportunity are higher.

The EU is not losing the AI race because Europeans aren’t smart enough. They’re losing it because the institutional and financial infrastructure for frontier AI development doesn’t exist at European scale.

China’s Patent Paradox

Here’s a number that should make you pause: China filed 38,210 generative AI patent inventions between 2014 and 2023, six times the US total of 6,276. China is filing more AI patents than anyone else in the world. Yet its private AI investment is 23 times smaller than the US. What explains this paradox?

Two things. First, patent quantity and patent quality are very different metrics. Many Chinese AI patents cover incremental improvements or applications, while US patents tend to cover foundational model architectures and infrastructure. Second, China’s AI development is heavily state-directed rather than venture-funded, which produces different outputs, more applied AI in manufacturing, surveillance and logistics, less foundational research.

China’s strategic goal of becoming the world’s leading AI nation by 2030 is genuine, and its progress in specific domains, particularly computer vision, autonomous vehicles and smart manufacturing is real. But the overall investment gap makes that goal increasingly difficult to achieve on the current trajectory.

What This Means for the Global Economy

From a macroeconomic perspective, the AI investment race has profound implications for long-run growth.

The Solow Growth Model tells us that sustainable economic growth ultimately depends on technological progress, improvements in total factor productivity that allow economies to produce more from the same inputs. AI represents exactly this kind of productivity-enhancing technology.

The INSEAD faculty survey found that AI inequalities will help advanced economies boost productivity at twice the rate of lower-income countries. Countries that lead in AI investment today are essentially front-loading decades of future productivity growth. Countries that fall behind face not just a temporary disadvantage, but a structural shift in their long-run growth potential.

This is why the AI investment gap matters far beyond the technology sector. A world where one country captures the majority of AI-driven productivity gains is a world of accelerating economic divergence and more inequality between nations, not less.

The Ground Floor Take

The global AI investment race in 2025 is simultaneously the most important and most lopsided economic competition of our time. The US leads by a margin so large that catching up through conventional investment alone seems impossible in the near term. China is the only country operating at anything approaching comparable scale, and even it trails by a 23x multiple. Everyone else is competing for influence at the margins.

But the outlier stories of UAE, Singapore, India suggest that the race isn’t purely about who spends the most. Strategic deployment, regulatory frameworks, and national AI strategies can allow smaller players to punch above their weight in specific domains.

The deeper question is whether the current investment gap translates into a permanent productivity and economic power gap or whether AI, like previous general-purpose technologies, eventually diffuses globally and lifts all economies.

History offers some comfort. Electricity and the internet both started with massive geographic concentration before spreading worldwide. But both also took decades to diffuse, and the countries that led early captured enormous and lasting advantages.

The race is not over. But the starting positions are very unequal and getting more so every year.

Is the global AI investment gap a temporary phenomenon that will self-correct, or are we watching the formation of a permanent new economic hierarchy? What do you think?