On June 12, 2026, something unprecedented happens. A company that builds rockets, runs the world’s largest satellite internet network, and is burning billions developing artificial intelligence will begin trading on the Nasdaq under the ticker SPCX. SpaceX, the company Elon Musk founded in 2002 with the stated goal of making humanity multiplanetary is going public at $135 per share, seeking to raise $75 billion and carry a valuation of $1.77 trillion. To put that number in perspective: it would make SpaceX larger than every company in the S&P 500 except six. It would more than double Saudi Aramco’s 2019 record of $29 billion the previous largest IPO in history. And it would give public investors their first chance to own a piece of one of the most consequential private companies ever built.

The financial picture behind that IPO valuation, however, is far more complicated than the headline suggests.

Understanding the IPO Mechanism

To appreciate what SpaceX is doing, you first need to understand how IPOs work and how SpaceX has broken from convention at almost every step.

Book Building: The Standard Process

In a conventional IPO, the process works like this: the company files an S-1 registration statement with the Securities and Exchange Commission disclosing its financials, then embarks on a roadshow where management presents to institutional investors across major financial centers. Based on the demand signals gathered during the roadshow, underwriters set a price range. Orders come in. The final price is set within that range the night before listing. The stock begins trading the following morning. This process is called book building, it exists to discover the market-clearing price. It creates a feedback loop between the company’s ambitions and what institutional investors are actually willing to pay.

SpaceX did something different. Rather than launching with a price range and letting the market narrow it, SpaceX went straight to a fixed price of $135 per share. No range. No negotiation. No traditional bookbuild. The company handed the market a number and moved on, a signal of either extraordinary confidence in demand or a deliberate anchoring strategy.

The Underwriting Syndicate

Behind every major IPO is a syndicate of banks that underwrite the offering meaning they commit to selling the shares and, in some structures, to buying any unsold inventory. SpaceX has assembled 21 banks, with Goldman Sachs as lead left bookrunner and Bank of America, Citigroup, JPMorgan Chase, and Morgan Stanley as senior co-bookrunners. The size of the syndicate reflects the size of the deal, distributing $75 billion in shares requires an enormous network of institutional relationships. Underwriters earn fees, typically 3-7% of the total raise making this one of the most lucrative single transactions in investment banking history.

The Retail Allocation: A Strategic Choice

Perhaps the most unusual feature of the SpaceX IPO is its retail allocation. SpaceX has reserved 30% of the float for retail investors, which is three times the standard allocation for a company of this size. In most mega-cap IPOs, retail investors get 10% or less, with the bulk going to institutional investors like pension funds, sovereign wealth funds, and hedge funds.

Why give retail so much access? The calculus is strategic. Millions of small shareholders create a natural constituency of supporters, people who have a financial stake in SpaceX’s success and are less likely to sell at the first sign of volatility. It also generates enormous media coverage and public goodwill, which matters for a consumer-facing business like Starlink. And in an era of political scrutiny of Big Tech, a company whose shareholders include everyday Americans from across the country has a different political profile than one owned primarily by institutional investors.

The Bridge Loan Overhang

One critical detail that deserves more attention than it typically gets in coverage of this IPO: SpaceX currently carries $29.1 billion in long-term debt, including a $20 billion bridge loan it intends to repay at least partially from IPO proceeds within six months. This means a significant portion of the $75 billion being raised is not going toward growth investment, it is going toward debt repayment. When evaluating an IPO, the use of proceeds is a fundamental analytical consideration. Investors should understand that they are partly refinancing existing obligations, not purely funding future growth.

Dissecting the Business

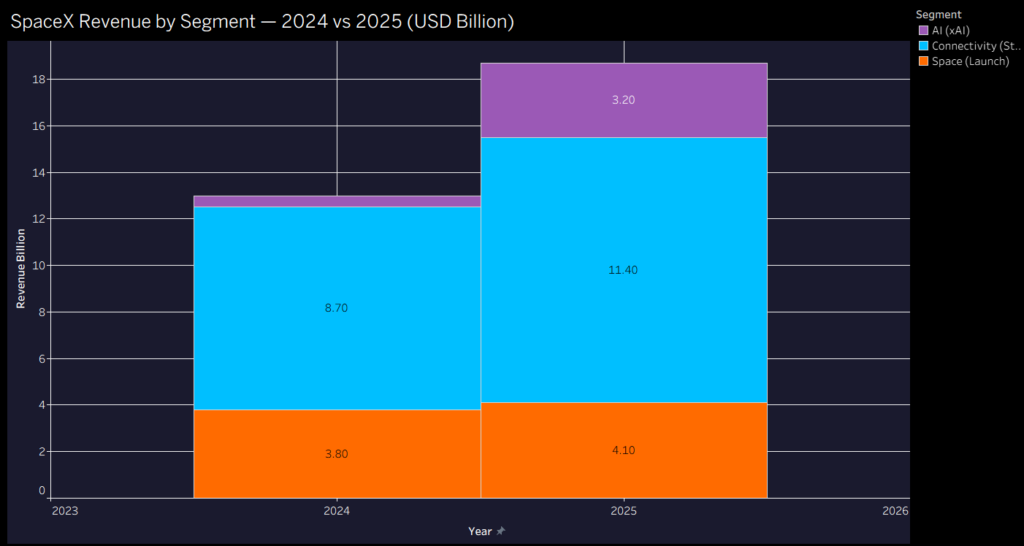

Here is the detail that makes SpaceX financially unusual: what is being sold to the public is not simply a rocket company. In February 2026, SpaceX merged with Elon Musk’s xAI, the company behind the Grok large language model and the X social media platform, in a common-control transaction. Under Generally Accepted Accounting Principles accounting rules, because Musk controlled all three entities, the financials have been restated as if they were always one company.

What investors are actually buying is three distinct businesses with very different financial profiles:

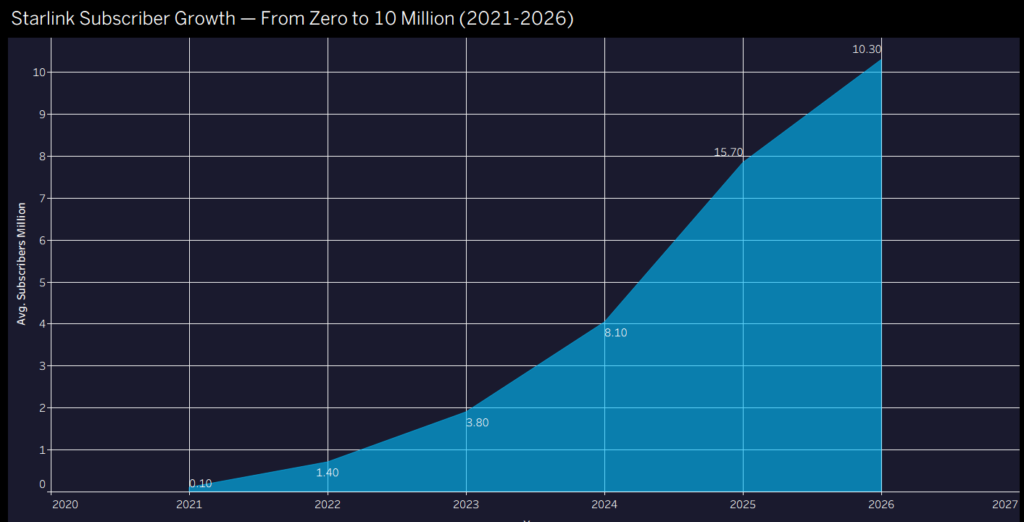

Connectivity (Starlink): The satellite internet business is SpaceX’s crown jewel and its only profitable segment. Starlink generated $11.4 billion in revenue in 2025, approximately 61% of total company revenue and produced $4.4 billion in operating profit. Subscriber growth has been remarkable: from 2.3 million users in 2023 to 8.9 million at end of 2025, reaching 10.3 million by Q1 2026. This is a genuine, recurring-revenue business with real competitive moats.

Starlink Subscriber Growth 2021-2026. Source: SpaceX S-1 Filing

Space (Launch Services): The rocket launch and payload business generated $4.1 billion in revenue in 2025, primarily from Pentagon and NASA contracts, but was loss-making due to increased costs linked to Starship development. Revenue growth has slowed to 8% year-over-year as the market matures. Starship, SpaceX’s next-generation heavy-lift rocket is the key to future growth in this segment, but its development timeline carries significant uncertainty.

AI (xAI): The AI segment generated $3.2 billion in revenue in 2025 but produced a $6.4 billion operating loss. xAI is burning approximately $2.5 billion per quarter as it builds out compute infrastructure, trains large language models, and attempts to scale the Grok platform. This segment is, by any conventional financial measure, a massive cash drain.

The consolidated picture: $18.7 billion in revenue in 2025, growing 33% year-over-year, with a net loss of approximately $4.94 billion.

SpaceX Revenue by Segment 2024 vs 2025 (USD Billion). Source: SpaceX S-1 Filing, May 2026

The Valuation

At $1.77 trillion for a company with $18.7 billion in revenue and a nearly $5 billion net loss, SpaceX is trading at approximately 95x revenue. This is where the most important analytical work happens.

Valuation Method 1: Price-to-Earnings (P/E)

The P/E ratio is the most commonly used valuation metric in equity markets. It divides a company’s market capitalization by its annual net earnings to show how much investors are paying for each dollar of profit.

SpaceX’s P/E ratio cannot be calculated because SpaceX has no earnings. It is deeply loss-making. When a company has negative earnings, the P/E ratio is undefined, which is itself an important signal. Investors are being asked to value not current profitability, but future profitability a significantly more speculative exercise.

Valuation Method 2: EV/EBITDA

Enterprise Value to EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is a popular alternative for capital-intensive businesses where net income is distorted by large depreciation charges. SpaceX’s adjusted EBITDA grew 23% in 2025, driven almost entirely by Starlink’s 86% EBITDA improvement. However, group adjusted EBITDA fell 35% in Q1 2026 as xAI losses accelerated. Capex is one of the clearest signs of where SpaceX is putting money to work, most of the near-term spending is being directed toward scaling the AI segment. With $10.1 billion in Q1 2026 capex alone, free cash flow is deeply negative, making EV/EBITDA multiples extremely elevated.

Valuation Method 3: DCF (Discounted Cash Flow)

A DCF model values a company based on the present value of its projected future cash flows, discounted back at a rate that reflects the risk of those cash flows materializing. It is the most theoretically rigorous valuation method and the one that requires the most assumptions.

The bull case DCF for SpaceX runs something like this: Starlink reaches 50 million subscribers by 2030 (roughly 5% of the global broadband market) at an improving ARPU following the recent price increases. The launch business recovers as Starship becomes operational and opens new revenue streams. xAI begins generating meaningful revenue from enterprise AI contracts and compute infrastructure. Orbital AI compute and data centers in space becomes a viable business by 2032. At a 10% discount rate and aggressive growth assumptions, this DCF can support a valuation in the $1.5-2 trillion range.

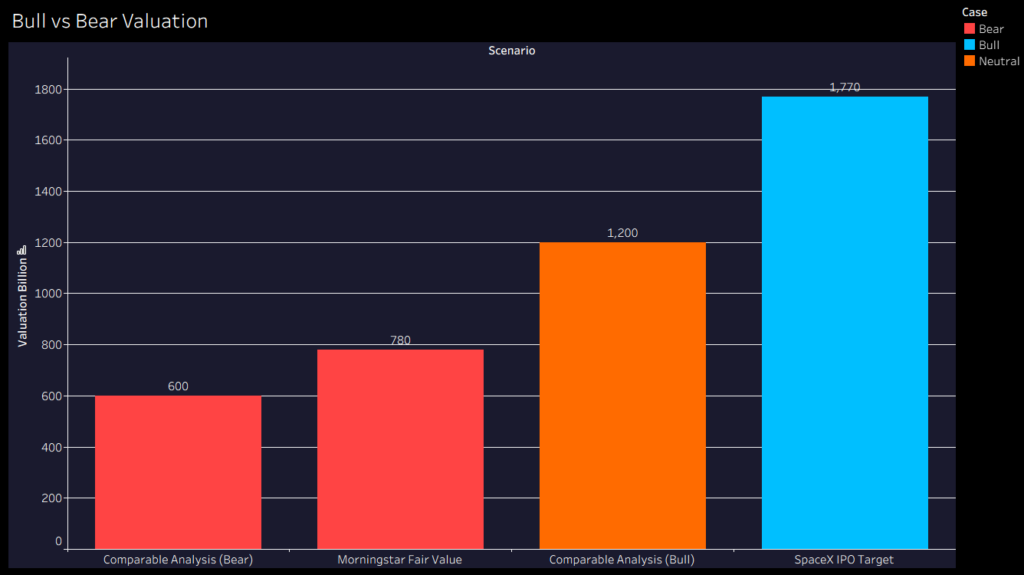

The bear case DCF runs like this: Starlink’s ARPU has already declined from $99 per subscriber per month in 2023 to $66 by end of Q1 2026, a 33% decline even as the subscriber base quadrupled, reflecting intense competitive pressure and a shift to lower-value markets. xAI’s losses accelerate before they reverse. Starship faces continued delays. Orbital compute remains speculative. At a 12% discount rate and conservative growth assumptions, Morningstar arrives at a fair value of $780 billion, 56% below the IPO price.

The honest answer is that both DCFs are defensible, and the spread between them tells you everything about the uncertainty embedded in this valuation.

SpaceX Valuation Scenarios — Bear to Bull Case (USD Billion). Source: Morningstar, Ground Floor Analyst Analysis

Comparable Company Analysis

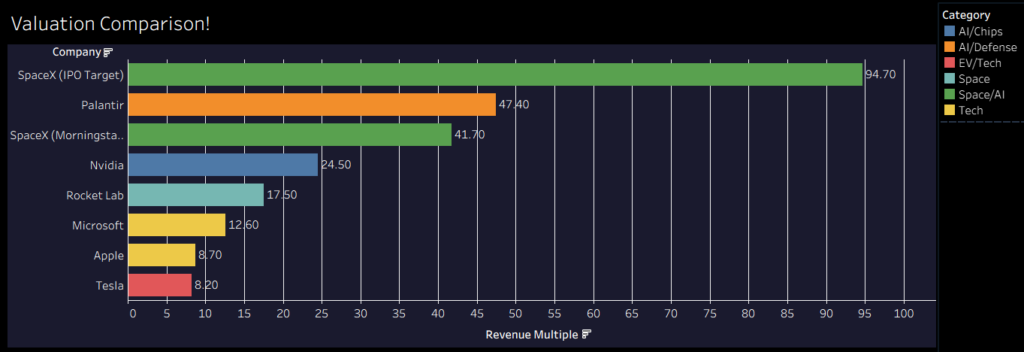

Looking at public comparables provides useful context even if no single company is a perfect match. Rocket Lab trades at approximately 15-20x revenue for its launch business. Viasat trades at 2-3x revenue for satellite communications. Palantir perhaps the closest AI infrastructure comparable trades at 40-50x revenue. A blended comparable analysis across SpaceX’s three business segments produces a range of $600 billion to $1.2 trillion, well below the IPO valuation in every scenario. Morningstar’s $780 billion estimate sits in the middle of this range.

The premium above comparable company valuations represents the market’s pricing of SpaceX’s unique competitive position, Starlink’s network effects, and the optionality embedded in its longer-term ambitions.

Revenue Multiple Comparison — SpaceX vs Global Tech Giants. Source: Ground Floor Analyst Analysis

What Retail Investors Are Really Buying

Here is the most important thing retail investors need to understand before buying SPCX: the shares being offered in the IPO are Class A shares. Elon Musk holds Class B and Class C shares that carry dramatically different voting rights. Musk owns 42% of SpaceX’s equity but controls 85% of its voting rights. This means that regardless of how many shares the public owns, public shareholders have essentially no ability to influence company decisions. They cannot vote to change the board. They cannot vote against executive compensation. They cannot push back against related-party transactions.

In corporate governance terms, this is a classic principal-agent problem operating at an extreme. The principals (public shareholders) have entrusted capital to an agent (Musk) whose interests, priorities, and time horizons may not align with theirs. And uniquely among dual-class structures, this agent has stated publicly that his primary motivation is not financial return but the long-term survival of humanity, including a stated desire to colonize Mars. His compensation plan is explicitly tied to milestones related to a Mars colony.

This is not a criticism of Musk’s ambitions. It is an observation that investors who buy SPCX are making a bet not on a company with conventional corporate governance, but on a single individual’s vision, judgment, and continued engagement.

The Ground Floor Take

The SpaceX IPO is unlike any public offering that has come before it, not just in scale, but in complexity, ambiguity, and the sheer breadth of what it asks investors to believe.

The foundation is real and impressive. Starlink’s 86% increase in adjusted EBITDA between 2024 and 2025, its 10 million subscribers across 160 countries, and its position as the world’s dominant satellite internet network represent genuine, defensible business value. The launch business has a competitive moat that has taken two decades and billions of dollars to build. These are not speculative assets.

But the valuation of $1.77 trillion asks investors to pay for much more than what exists today. It asks them to pay for orbital AI compute that doesn’t yet exist, for xAI becoming competitive with OpenAI and Google, for Starlink reaching hundreds of millions of subscribers globally, and for Starship unlocking cost curves that make current projections look conservative.

Each of these outcomes is possible. None of them is certain. And the governance structure means that investors who disagree with how Musk pursues these outcomes have no mechanism to express that disagreement except by selling their shares. The SpaceX IPO is ultimately a referendum on whether you believe Elon Musk’s vision of the future is worth $1.77 trillion today. Markets will give their answer on June 12.

Would you buy SpaceX at $135 per share? Is the $1.77 trillion valuation a fair price for the future or the most expensive bet in market history?