The BIS just flagged AI as a systemic financial risk. Here’s why that matters more than anything Elon Musk tweeted this week.

There is a hierarchy to financial warnings. When a retail investor on Reddit says the market is overvalued, you scroll past. When a Wall Street analyst issues a cautious note, you note it and move on. But when the Bank for International Settlements, the institution that literally serves as the central bank for the world’s central banks publishes its annual economic report and using phrases like ‘protracted investment bust,’ and “systemic risk,” you stop and read it carefully. BIS warns that the AI bubble burst risk is now a central concern for the institution with the clearest view of global financial plumbing.

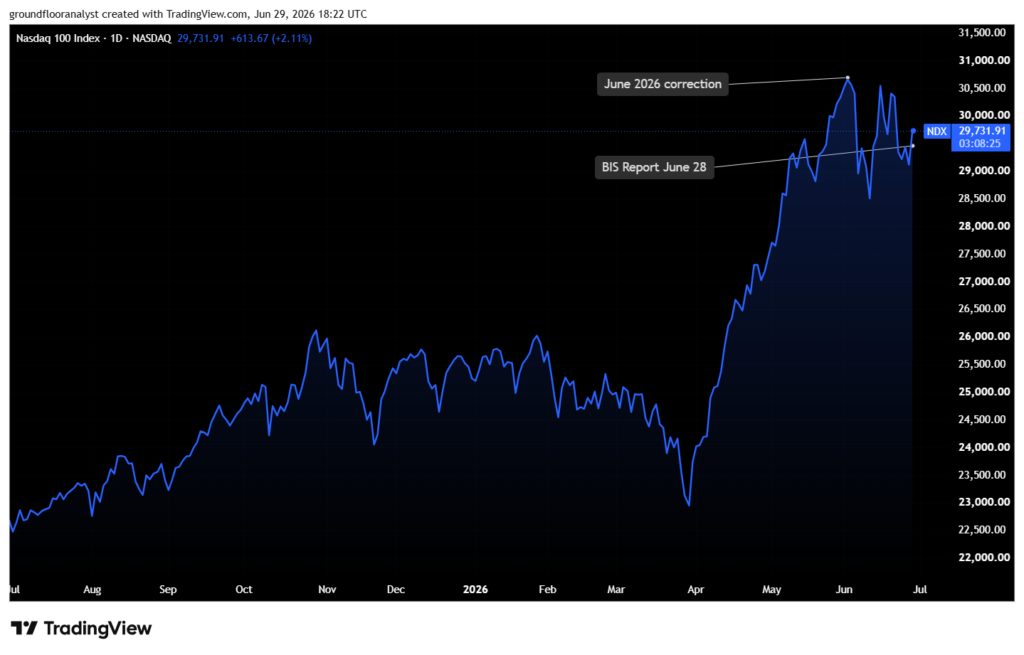

On June 28, 2026, the BIS did exactly that. Its annual economic report identified three interlocking pressure points threatening global financial stability: an AI investment bubble, persistent inflation, and a sovereign debt time bomb. The AI warning was not a footnote. It was a central argument in a report that the world’s most senior monetary policymakers will spend the next several months digesting.

The question worth asking is not whether the BIS is right. It is why, if the risks are this visible to the institution with the clearest view of global financial plumbing, the money keeps flowing anyway.

Minsky Was Here First

To understand what the BIS is actually warning about, you need Hyman Minsky. An economist whose most important work was largely ignored, until 2008 proved him correct.

Minsky’s Financial Instability Hypothesis argues that stability itself is destabilising. In periods of economic calm, investors gradually take on more risk. Lending standards loosen. Asset prices rise. Rising prices justify further borrowing. The cycle feeds itself until the system reaches what became known as a “Minsky Moment”, the point at which the debt burden can no longer be serviced by income, and the whole structure unwinds suddenly and violently.

Minsky identified three stages of borrower behaviour. “Hedge financing” where income covers both interest and principal is the safe stage. “Speculative financing” where income covers interest but not principal, requiring constant refinancing is the fragile stage. “Ponzi financing” where income covers neither, and borrowers rely entirely on asset price appreciation to survive is the dangerous stage.

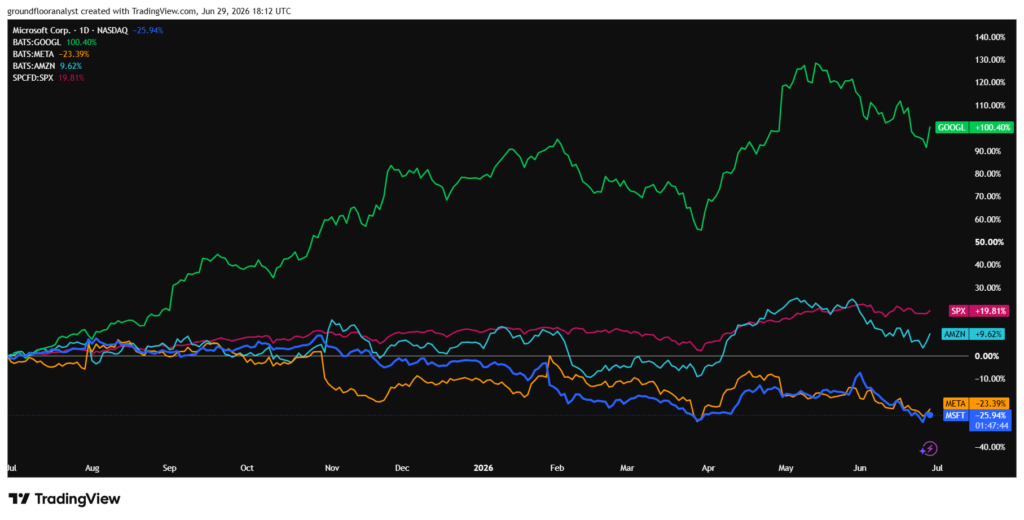

The BIS report is, in effect, arguing that parts of the AI investment ecosystem have moved into Minsky’s third stage. The five largest hyperscalers are set to spend more than a trillion dollars on AI-related capital expenditure through 2026, a commitment that is already outpacing their earnings and free cash flow. The gap is being filled by debt issuance, corporate bonds issued against the promise of future AI returns that have not yet materialised.

The Circular Financing Problem Fueling the AI Bubble Burst Risk

The Minsky diagnosis is serious. The circular financing problem is worse, because it means the revenue numbers being used to justify the AI buildout may not be as clean as they look on a balance sheet.

Here is how it works: a hyperscaler say, Microsoft takes an equity stake in an AI lab say, OpenAI. That AI lab then commits to buying its compute infrastructure from Microsoft’s Azure cloud platform. Microsoft records that as cloud revenue. OpenAI records the Azure spend as an operating cost. The equity stake creates alignment. The revenue looks real. The growth chart looks strong.

The BIS flagged this structure explicitly in its June 28 report, noting that hyperscalers’ announced multi-year compute commitments were widespread as of April 2026. The problem is straightforward: if a meaningful portion of hyperscaler AI revenue is flowing from companies in which the hyperscalers themselves hold equity stakes, then the revenue is partially circular. It is not entirely new demand from external customers. It is, in part, money moving around inside a closed loop and being counted as growth at each transfer point.

This is not fraud. It is not even unusual in early-stage technology ecosystems. But it does mean that the headline AI revenue figures that analysts and investors are using to justify trillion-dollar valuations may be overstating genuine external demand. The BIS is essentially pointing at the revenue chart and asking: how much of this is real?

What a DCF Actually Tells You

The valuation question brings us to the most grounding exercise available in finance: a discounted cash flow analysis. DCF strips away narrative and forces you to answer one specific question, what does this asset need to earn, over what period, at what growth rate, to justify what you are paying for it today?

Run a DCF on Nvidia at its peak 2026 valuation and the numbers are instructive. At a market capitalisation of approximately $3.5 trillion and a discount rate of 10%, Nvidia needs to grow its free cash flow at roughly 25-30% annually for the next decade to justify current pricing and then maintain double-digit growth for a decade after that. This is not impossible. It is also not guaranteed. The margin for disappointment is essentially zero.

The BIS makes this point implicitly when it warns that “disappointment in returns could trigger a sudden pullback in financing.” In DCF terms, you do not need AI to fail for valuations to collapse. You need AI to underperform the extraordinary expectations already baked in. A shift from 30% annual FCF growth to 20% still exceptional by any historical standard, would imply a significant repricing of every asset in the AI ecosystem simultaneously.

That is what makes the current moment different from standard bubble analysis. The question is not whether AI will create value. It clearly will. The question is whether it will create value at the speed and scale implied by current market prices. If the answer is “probably yes, but slower,” the financial consequences are still severe.

Herd Behaviour and the Problem of Everyone Knowing

Behavioural finance adds a layer to this that pure DCF analysis misses. Even investors who privately believe AI valuations are stretched have a rational incentive to keep investing because the cost of being early to exit is being left behind during the final phase of the rally, and the cost of being last to exit can be absorbed by finding someone else to sell to.

This is classic herd behaviour: individually rational decisions that produce collectively irrational outcomes. Every fund manager who continues to hold Nvidia above its intrinsic value is making a defensible choice in isolation. They are also participating in a collective dynamic that makes the eventual correction sharper than it would otherwise be.

The BIS is uniquely positioned to see this from above. It has visibility into non-bank financial institution positioning, sovereign debt market fragility, and private credit exposure that no individual fund manager possesses. When it describes non-bank institutions now holding 53% of sovereign debt, up from 44% in 2021, it is identifying a structural change in who bears the risk when financial conditions tighten. Hedge funds, money market funds, and open-ended bond funds do not behave like bank balance sheets. They face redemption pressure. They sell when volatility spikes. That selling can cascade.

The BIS is not saying the crash is coming next Tuesday. It is saying the financial system has quietly reorganised itself in ways that make the transmission of a shock faster and broader than it was in 2019.

The Ground Floor Take

The BIS is not a doomsday institution. It does not issue warnings for attention. When it uses the words “systemic risk”, it is choosing those words carefully.

The honest reading of the June 28 report is this: AI is real, the productivity gains are real, and the long-term case for the technology is intact. But the financial structures wrapped around AI, the circular financing, the debt-funded capex, the leveraged non-bank holders of sovereign debt sitting underneath all of it are not as clean as the revenue charts suggest. The emperor is wearing clothes, just fewer of them than the market is currently pricing.

Canals were real infrastructure that transformed the British economy. The British railway boom of the 1840s was real technology that reshaped commerce. The internet was real and did change everything. All three still produced devastating financial crashes during their buildout phases, because the pace of capital deployment outran the pace of return generation.

AI may be different this time. It may generate returns fast enough, broadly enough, to justify the current pace of spending. But “may be different this time” are the four most expensive words in finance. The BIS just reminded us why.